Greece's payment ecosystem has undergone a quiet but significant transformation over the past few years. At the centre of that shift is IRIS – an instant bank-to-bank payment network that has moved from a niche digital convenience to a mandatory fixture of commercial life. With over 4.25 million active users, €11 billion in projected annual transaction value, and a new legislative mandate requiring all businesses to accept it, IRIS payments in Greece now represent one of the most consequential local payment developments in Southern Europe.

Key figures at a glance by the end of 2025:

| Metric | Figure |

| Active users | 4.25 million |

| Registered professionals | 583,445 |

| POS terminals supporting IRIS | ~1.2 million |

| E-shops supporting IRIS | 70,000 |

| Total transaction value | €10.9 billion |

| Mandatory for | All B2C transactions in Greece |

| Minimum fine for non-compliance | €1,500 |

| Daily P2P / P2B limit | €1,000 |

| Monthly P2P limit | €5,000 |

Source: Dias, 2026

What is IRIS payment in Greece?

IRIS is an instant bank-to-bank payment service developed in 2017 and operated by DIAS Interbanking Systems S.A., Greece's central interbank payment infrastructure provider. It enables individuals and businesses to send and receive money in real time – directly between bank accounts – without the need for card details or IBAN numbers.

IRIS payments in Greece are built on the European SEPA Instant Credit Transfer (SCT Inst) standard, meaning they comply with EU-wide rules for fast, secure, and irrevocable transactions. Settlement is immediate, funds are available within seconds and the system operates around the clock, every day of the year.

The name "IRIS", beyond its reference to the Greek messenger goddess, reflects the system's role as a connector: between individuals, between consumers and businesses and increasingly, between Greece and the rest of Europe.

How is IRIS different from other European local payment methods?

Unlike some European local payment methods that rely on one-time codes (like BLIK in Poland), standalone wallets (like Satispay in Italy), or checkout-only redirects (like iDEAL in the Netherlands), IRIS works directly through a user's existing banking app with no separate account to manage. In this way it is closer in spirit to Swish (Sweden) or MBWay (Portugal).

This architecture has practical implications: adoption is driven by banking penetration rather than standalone app installs, and trust is inherited from established financial institutions rather than built from scratch.

What makes IRIS in Greece unique?

What distinguishes IRIS from most equivalent systems in Europe is its legal status. Most instant payment schemes operate on a voluntary basis – merchants choose whether to accept them based on business appetite. In Greece, that choice has been removed.

Local laws established a binding obligation for all businesses and legal entities registered in Greece to offer IRIS as a standard payment option. The mandate covers every type of commercial entity – from sole traders and street vendors to large retail chains and service providers. Full enforcement came into effect on 1 December 2025, and businesses that fail to provide IRIS as a checkout option face fines starting at €1,500.

This legislative push is primarily motivated by Greece's long-running effort to combat tax evasion and increase fiscal transparency. By funnelling commercial transactions through a traceable, real-time digital system, the government gains significantly better visibility into the flow of money through the economy.

The result is a payment method with unusually strong merchant coverage – driven not only by consumer demand but by regulatory compulsion.

Does it mean that international sellers operating in Greece must offer it too?

The short answer is: No, it is generally not mandatory – provided your business is not legally established in Greece and you do not have a Greek Tax Identification Number (AFM).

That said, with over 4.25 million active users and its growing role in everyday transactions, businesses with meaningful exposure to Greek consumers may find it worth offering regardless.

Where Does IRIS Work? Use Cases

IRIS operates across four distinct payment contexts, each with its own mechanics and applicable limits.

IRIS P2P: Person-to-Person Transfers

IRIS P2P allows individuals to send money instantly to other people using a mobile phone number, and in some cases email address as a proxy to bank account. There is no need to exchange IBAN details. Transfers are free of charge for the sender and execute in real time via the user's banking app.

| Limit type | Amount |

| Daily outgoing limit | €1,000 |

| Monthly outgoing limit | €5,000 |

| Per transaction | Up to daily limit |

The daily limit was doubled from €500 to €1,000 in January 2026 to accommodate larger personal transfers such as rent contributions or shared household bills.

IRIS P2B: Payments to Freelancers and Professionals

The P2B (Person-to-Business/Professional) variant is designed for freelancers, sole traders and self-employed professionals – doctors, lawyers, tradespeople and similar service providers. Clients can initiate a payment by scanning the professional's static IRIS QR code or by entering their Tax Identification Number (AFM) or mobile number.

Payment is free for the payer. Fees for the professional receiving funds are determined by their bank contract.

| Limit type | Amount |

| Daily incoming (professional) | €10,000 |

| Monthly incoming cap | None |

| Per transaction | Up to €1,000 |

IRIS Commerce: Online Payments

For e-commerce, IRIS Commerce operates via a bank redirect flow. At checkout, the customer selects IRIS, is taken to their banking app to confirm the payment and is returned to the merchant's site. Settlement is instant and final – unlike card payments, there is no chargeback mechanism.

Merchants integrate IRIS Commerce through a local acquiring bank or a Payment Service Provider (PSP). Documented options include Nexi XPay Greece, Viva.com, Worldline, NBG Pay, Everypay, and Adyen (through a Greek acquiring bank). Depending on the provider, integration is available via hosted payment pages, API, e-commerce plugins or mobile SDK.

No product-level transaction limit applies to IRIS Commerce though individual banks may apply their own security thresholds based on customer profile.

IRIS Commerce: In-Store / Retail Payments

At physical points of sale, IRIS Commerce uses dynamic QR codes – unique to each transaction – generated by the POS terminal. The consumer scans the QR code with their banking app, authenticates and confirms payment. The merchant receives instant notification and irrevocable settlement.

How does IRIS work for the payer?

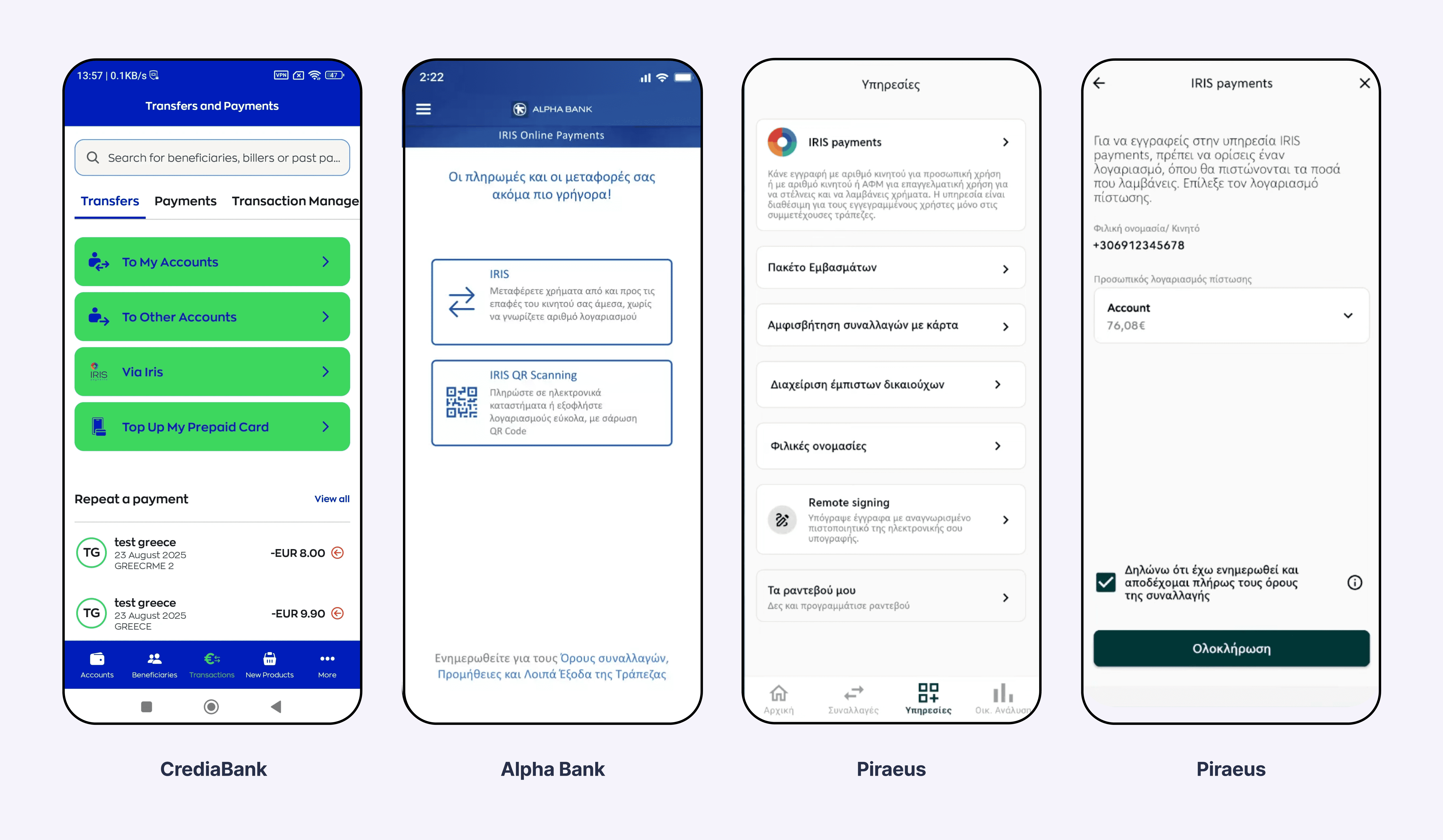

From the consumer's perspective, IRIS requires no new apps, no registration beyond what their bank already provides and no learning curve beyond the initial setup of an alias (mobile number or email) linked to their account. All interaction happens within the familiar interface of their existing mobile banking app but also means that the execution varies by the bank.

For example, below are screens from the IRIS payment experience across three Greek banking apps: CrediaBank, Piraeus and Alpha Bank.

Sources: CrediaBank via Google Pay; Alpha Bank website; Piraeus via Youtube

How popular are IRIS payments in Greece?

The aggressive rollout of IRIS has produced significant shifts in the Greek financial landscape.

By late 2025, instant payments accounted for approximately 40% of all credit transfers in Greece – a figure that substantially exceeds the Eurozone average. DIAS, the operator of the system, reported 122.1 million instant payment transactions in 2025, representing a 72.8% year-on-year increase and accounting for 27% of total credit transfers across all DIAS payment systems.

P2P activity has been particularly explosive. In Q1 2025 alone, P2P transactions reached 17.5 million – a 98.3% increase compared to the same period in 2024. IRIS Commerce volumes grew by 70.8% year-on-year in 2025 and are now sixteen times higher than they were in 2020.

The Future of IRIS: Cross-Border Expansion via EuroPA

The most significant development on the horizon for IRIS payments in Greece is the country's participation in the EuroPA network – a cross-border alliance of national instant payment schemes that includes Bizum (Spain), Bancomat Pay (Italy), MB WAY (Portugal), and Vipps MobilePay (Nordic countries).

The rollout is structured in two phases:

- Mid-2026 (Initial Phase): Greek users will be able to initiate instant P2P transfers to individuals in Spain, Italy, and Portugal directly from their Greek banking app, using the same alias-based flow (mobile number / QR) already used domestically.

- Late 2026 (Commercial Expansion): Visitors from EuroPA member countries will be able to pay Greek merchants using IRIS QR codes via their own domestic apps – meaning a Spanish tourist could pay at a Greek restaurant using Bizum, or a Portuguese visitor could settle a hotel bill via MB WAY, with the transaction settling through the IRIS infrastructure on the merchant side.

IRIS is also expected to become interoperable with Wero, the pan-European payment scheme backed by major Western European banks, which would extend its reach into Germany, France, and Belgium.

Final Thoughts

IRIS has followed an unusual trajectory among European local payment methods: it did not grow to dominance through consumer enthusiasm alone, but through a combination of genuine utility, strong network effects within the Greek banking system, and – ultimately – legislative mandate. The result is a payment infrastructure with near-universal merchant coverage, deep consumer adoption and a transaction volume curve that shows no signs of flattening.

This article is provided for general informational purposes only.

FAQs

What banks support IRIS payment?

All major Greek banks participate in the IRIS network, including Alpha Bank, National Bank of Greece, Eurobank, Piraeus Bank, Cooperative Bank of Epirus, Vivabank, Optima Bank, Credia Bank, Snappi, Cooperative Bank of Thessaly, Cooperative Bank of Karditsa and Cooperative Bank of Chania.

What is iris pay in Greece?

IRIS pay is Greece's national instant payment system, operated by DIAS Interbanking Systems. It enables real-time, bank-to-bank transfers between individuals and businesses using a mobile number, email, QR code, or tax ID – with no card details or IBAN required.

Is IRIS Greece payment safe?

Yes. IRIS Greece payment is built on the EU's SEPA Instant Credit Transfer (SCT Inst) standard and regulated under Greek and European banking law. Transactions are authenticated through the user's own bank – using the same security layer (PIN, biometrics, or 2FA) as their regular mobile banking.

Latest from Noda

Instant Payment Systems Around the World: A Global Guide for Businesses

Open Banking in Malta: A Guide for 2026

IRIS in Greece: an overview of the local payments landscape