Open banking has long become a power actively changing how businesses and consumers interact with financial services. What started as a regulatory push in Europe has now grown into a global movement, bringing more intuitive, comfortable payments and data insights to customers and merchants.

As adoption across Europe (and the world) rises, with new technologies like AI reshaping the fintech industry, each day brings new challenges and changes to the open banking ecosystem. In this article, we explore the key trends of open banking this year, and what they mean for merchants.

What Is Open Banking?

Open banking is a financial framework that allows traditional banks to securely share data with licensed third-party providers via application programming interfaces (APIs) with customer consent. In Europe, open banking started with the enforcement of PSD2 in 2018, which required banks to share APIs with authorised companies.

Open banking ended banks’ monopoly over customer data. With access to data, licensed providers can create new, innovative products and services such as payments, personalised data insights, aggregated account management, and more. Since its introduction, open banking has gained traction worldwide, transforming the world of fintech.

Key Open Banking Trends in 2026

In the following section we will examine the trends in open banking actively shaping the industry in 2026 and are set to influence the innovations in the future.

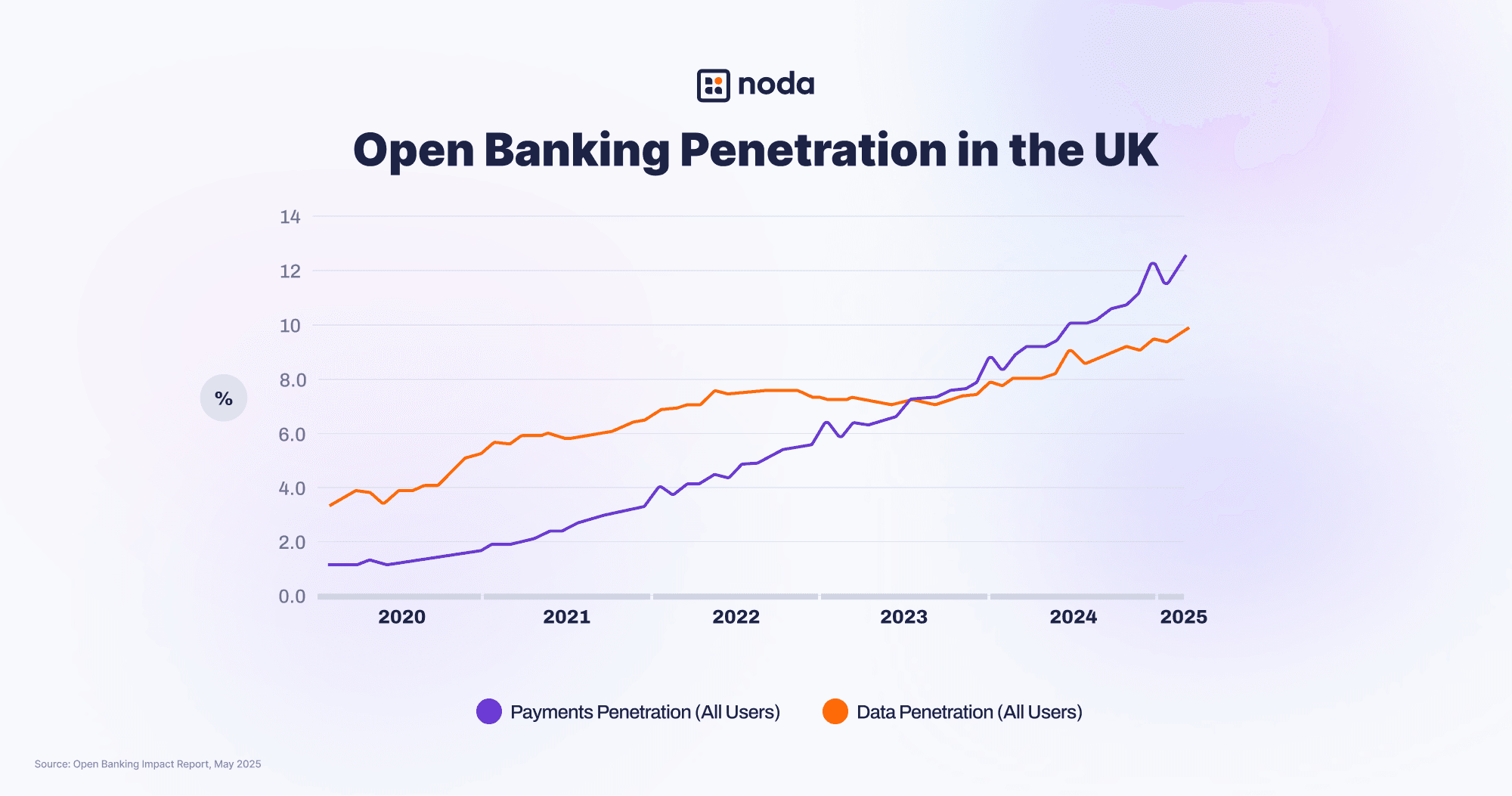

Growing Adoption and Market Maturity

Open banking continues to become more popular in Europe and globally. In the UK, for example, open banking has already moved into mainstream usage. In March 2025 alone, open banking payments comprised roughly 1 in 13 Faster Payments, with 70% year-on-year growth, and by the end of the year there were over 16.5 million user connections and 351 million open banking payments made.

18.4% of digitally active consumers and small businesses (1 in 5 users) were using open banking services, according to the Open Banking Impact Report published in May 2025. This marks a jump from mid-2023, when overall penetration stood at ~11% (1 in 9 users).

The market is expected to continue its growth both in the UK and beyond. Juniper Research forecasts global open banking API calls rising from 137 billion (2025) to >720 billion by 2029, even if adoption is uneven by region.

For businesses, the rapid maturing of the open banking market means greater opportunities to innovate. It’s also a chance to stay ahead in markets where open banking is quickly becoming a standard.

EU Instant Payments Regulation implementation

One of the most important developments shaping 2026 is the rise of instant euro payments as a baseline expectation, rather than a premium feature. The EU’s Instant Payments Regulation entered into force in 2024, but the major rollout milestones came in 2025, when banks in the euro area had to start supporting instant euro payments first for receiving and then for sending as well. By late 2025, instant euro payments had effectively become the new standard across the euro area, with the European Commission saying people and businesses can now send and receive them across every country in the eurozone.

This is a major step forward, and by now most banks serving private consumer accounts appear to have complied with the main requirements, even if implementation quality still varies between providers.

The challenge now is making this work smoothly and at scale across the wider payments ecosystem. While instant bank payments initiated through bank interfaces are becoming more common, there is still work to do to ensure the experience is consistent across all open banking implementations, including third-party apps and merchant payment journeys.

Commercial Variable Recurring Payments (cVRP)

Variable recurring payments, or VRPs, remain one of the most important recent open banking developments for businesses. While open banking is best known for one-off payments, where the customer approves each transaction, VRPs allow customers to authorise a provider to initiate multiple payments from their bank account within agreed limits. This makes them especially relevant for recurring but flexible payment scenarios.

In the UK, VRPs are already live for sweeping use cases, where customers move money between accounts they own. In 2026, the focus is starting to shift towards commercial VRPs, and we expect to see the first live use cases in lower-risk industries such as utilities, financial services and government.

Over time, this will become increasingly important as commercial VRP moves towards broader ecommerce adoption. This payment method could become a strong alternative to cards and direct debit for subscription businesses, utilities, telecoms, insurance, SaaS, and multiple other business models based on recurring payment flows.

Wero and Europe’s Push for Payment Sovereignty

Europe’s drive to reduce reliance on global card rails and non-European payment solutions is becoming more visible, and Wero is a good example of that trend. Developed by the European Payments Initiative, Wero is a new digital wallet linked directly to bank accounts, with the aim of supporting peer-to-peer, online and later in-store payments across Europe. By late 2025, EPI said Wero was already used by over 45 million Europeans.

A big part of Wero’s focus in 2026 is expansion strategy working with local methods. Some established ones are transitioning into Wero: both Netherland’s iDEAL and Payconiq, popular in Belgium and Luxembourg, are being folded into the broader Wero model. At the same time, other domestic schemes are expected to keep their local brands while working towards interoperability with Wero, including Bizum in Spain, Bancomat in Italy, MB WAY in Portugal and Vipps MobilePay in the Nordics.

Whether Wero becomes a dominant payment method remains to be seen. It is still in the early stages, with adoption so far focused mainly on peer-to-peer payments, although e-commerce rollout has started in some markets. Because this is a bank-led private-sector initiative, its long-term success will depend on broad participation from banks, merchants and local payment ecosystems.

Evolving regulations: PSD3 and PSR

Europe’s payments framework is still evolving. In November 2025, the Council and the European Parliament reached a provisional political agreement on the new Payment Services Regulation (PSR) and PSD3. The aim is to strengthen fraud prevention, improve transparency, modernise the rules for payment services and reduce some of the barriers that have made open banking inconsistent across EU markets.

For businesses, PSD3 and PSR matter less as a headline and more as a market-quality issue. In practice, the new rules should help improve API performance, clarify access rights, strengthen anti-fraud protections and make implementation more consistent across the EU. That should make open banking services easier to trust and easier to scale. In other words, regulation is increasingly focused on making the ecosystem work better in practice, not just opening the door in principle.

A major part of that is stronger fraud prevention and consumer protection. The provisional agreement puts a clear focus on tackling spoofing and scams, requiring payment providers to check that the payee’s name matches the account identifier, and supporting more fraud-related information sharing between providers.

Payments Lead Adoption, While Data Use Cases Broaden

Open banking is no longer just about moving money. Some of the most commercially relevant non-payment use cases in 2026 are digital identity, onboarding, affordability and fraud prevention. According to Open Banking Limited, around 80% of open banking API traffic is linked to Account Information Services (AIS), such as viewing balances and transaction histories. Open banking data is also increasingly being used to help businesses verify identity faster, reduce administrative burden and support use cases such as KYC, DBS checks and age assurance.

For merchants selling age-restricted products as well as for marketplaces, financial apps, lenders, travel providers and other platforms that may require stronger user verification, these use cases can be just as valuable as payments. In some cases, businesses use open banking data on its own. In others, they combine it with payment flows, for example by handling registration, age verification and the first payment in a single journey.

Either way, these services can improve conversion, reduce fraud losses, simplify compliance and make onboarding smoother. That makes open banking a broader business-enablement tool, not just a checkout method.

7. Open Banking Is Expanding Into Open Finance

Another major 2026 theme is that the industry is gradually moving beyond payment-account access toward open finance. The European Commission’s proposed Financial Data Access framework (FiDA) is intended to create a broader data-sharing model covering areas such as savings, investments, pensions, mortgages and insurance.

This is important because it changes the long-term strategic role of open banking. Instead of being limited to payments and current-account data, the model could eventually support much richer financial journeys across a wider range of products. That means that businesses like lenders, insurers, wealth platforms and personal finance apps could all use broader financial data to make decisions more accurately and deliver services that reflect a fuller picture of each customer’s financial situation.

That said, FiDA is still in the legislative phase, so 2026 is more likely to bring policy progress and industry preparation than real market rollout.

Conclusion

The picture that emerges from these trends is consistent: open banking is transitioning from a compliance exercise into commercial infrastructure. In the UK the adoption is at an all-time high, so the competitive question is no longer whether to participate but rather how well you execute. In the EU, the provisional agreement on PSD3 and PSR signals that regulators are done opening the door and are now focused on making the room functional: consistent API performance, mandatory fraud data-sharing, and liability that sits squarely with payment providers.

For merchants and fintechs, the era of treating open banking as an experiment is closing. Fraud controls, consent UX and reliability are becoming differentiators, and with FiDA on the horizon, the data layer will eventually extend well beyond payment accounts.

Latest from Noda

Gaming Payment Methods: Everything You Need To Know in 2026

Digital Payment Trends: Navigating the Future